Think of regulatory compliance risk management as the strategic game plan your organisation uses to spot, assess, and handle risks that pop up from not following laws, regulations, and even your own internal policies. It’s the critical navigation system that steers your business through a complicated sea of legal rules, helping you dodge hefty financial penalties, operational chaos, and serious damage to your reputation. This proactive mindset isn’t just a “nice-to-have” anymore; it’s absolutely fundamental for survival and growth.

Table of Contents

Why Regulatory Compliance Risk Management Is Not Optional

Imagine trying to captain a massive ship through a busy shipping lane where the maritime laws change daily without any warning. Navigating this journey without a top-notch navigation system and a sharp, vigilant crew would be more than just risky—it would be reckless. This is precisely the scenario modern businesses are up against, especially in a dynamic market like India.

Effective regulatory compliance risk management is that essential navigation system. It’s so much more than a box-ticking exercise to avoid fines. It’s about forging a resilient organisation that can weather legal storms, fiercely protect its brand, and maintain the solid trust of its customers and stakeholders.

The True Cost of Non-Compliance

Simply ignoring compliance risks opens the door to a flood of negative outcomes that go far beyond a simple fine. While the financial penalties can be staggering, it’s often the indirect costs that do the most long-term damage.

These hidden costs can be devastating:

- Reputational Damage: A single compliance slip-up can wipe out decades of brand trust almost overnight. News of data breaches or ethical missteps spreads like wildfire, pushing customers and partners away.

- Operational Disruption: Getting tied up in regulatory investigations or sanctions can bring business operations to a screeching halt, diverting critical resources and killing productivity.

- Loss of Business Opportunities: In today’s market, partners and clients are incredibly cautious about working with non-compliant businesses. This can lead directly to lost contracts and stunted growth.

For HR teams, the stakes are incredibly high. They are the guardians of incredibly sensitive employee data, from personal ID details to background verification results. A compliance failure here doesn’t just put the company in legal jeopardy under laws like the Digital Personal Data Protection Act; it shatters the trust of the entire workforce. This is why robust compliance is the absolute cornerstone of ethical, effective HR.

At its core, regulatory compliance risk management is about foresight. It’s the practice of looking ahead, anticipating potential legal and regulatory shifts, and building the necessary safeguards before they become urgent problems.

A Foundation for Growth and Trust

If you only see compliance as a defensive shield, you’re missing a huge opportunity. A strong risk management programme is actually a powerful tool for business growth. It sends a clear signal to the market that your organisation is stable, ethical, and well-managed, making you a far more attractive partner for investors, clients, and top-tier talent.

To really grasp the importance of managing all types of organisational risks, it’s helpful to look at the bigger picture. Reviewing a guide to risk management for businesses can provide a broader perspective. In our interconnected world, being proactive about compliance isn’t just about following the rules—it’s about setting your business up for sustainable, trustworthy growth. It’s the very bedrock on which a resilient and reputable company is built.

Building Your Compliance Framework from the Ground Up

A solid compliance framework isn’t some complex, mysterious beast. It’s really just a logical structure built on clear, actionable pillars. Think of it less like an abstract corporate policy and more like the architectural blueprint for a fortress designed to protect your organisation. A strong system for regulatory compliance risk management is built methodically, piece by piece, to withstand any external pressures.

This process rests on four essential pillars. By understanding how each one supports the others, you can build or reinforce a system that is both resilient and practical for your daily operations.

Pillar 1: Risk Identification

The first step is to actively hunt for potential gaps and weaknesses. This isn’t a passive activity where you just wait for problems to show up. It’s a proactive search, much like an engineer methodically inspecting a fortress wall for hidden cracks before an enemy can exploit them.

For an HR team, this means asking the tough questions:

- Where does our employee data live, and who has access to it?

- Are our background check procedures aligned with the latest legal standards in India?

- Could our hiring process unintentionally introduce bias?

This initial stage is all about mapping your entire operational landscape to pinpoint every single area where a regulatory or legal risk could materialise. If you don’t spot a risk at this stage, it goes unmanaged, leaving a dangerous blind spot in your defences.

Pillar 2: Risk Assessment

Once you’ve identified the potential risks, the next pillar is to assess their real-world impact. Let’s be honest, not all risks are created equal. A minor administrative error might be a small crack in the wall, but a major data breach could be a catastrophic structural failure.

Risk assessment involves looking at two key factors:

- Likelihood: How probable is it that this risk will actually happen?

- Impact: If it does happen, how severe will the consequences be for the business?

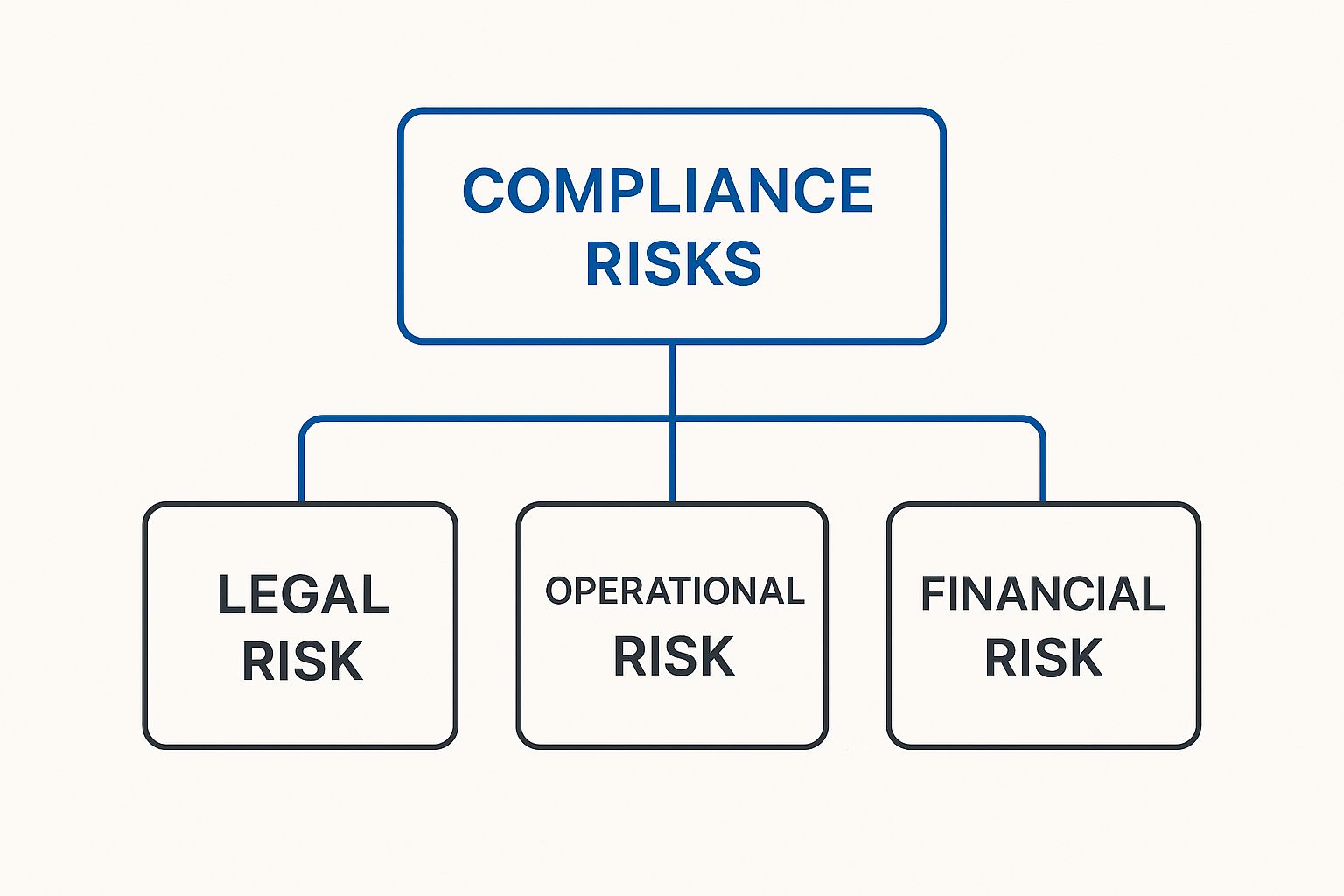

This analysis helps you prioritise what matters most. A high-likelihood, high-impact risk—like mishandling sensitive employee data under the Digital Personal Data Protection Act—demands immediate and robust attention. In contrast, a low-likelihood, low-impact risk can be managed with less intensive controls. The diagram below shows how compliance risks can manifest across different business areas.

As the infographic shows, a single compliance slip-up can ripple outwards, creating legal, operational, and financial damage all at once.

Pillar 3: Control Implementation

This is where you actually build your defences. Based on your risk assessment, you implement specific controls—the policies, procedures, and tools designed to neutralise the risks you’ve identified. This is the most tangible part of your regulatory compliance risk management framework.

Controls are the practical actions you take to reduce risk. They transform your strategy from a plan on paper into a living, breathing part of your organisation’s daily functions.

For example, if you spotted a risk related to inconsistent background checks, your controls might include:

- A formal background verification policy: This document clearly outlines when checks are required and what they must cover. No more guesswork.

- Partnering with a trusted verification service: Using a provider like SpringVerify ensures that all checks are thorough, consistent, and legally compliant, effectively outsourcing a major risk.

- Mandatory training for hiring managers: This makes sure everyone involved in hiring understands and follows the established procedures.

Pillar 4: Monitoring and Reporting

Finally, no fortress is complete without a watchtower. The fourth pillar, monitoring and reporting, is your organisation’s watchtower. It involves constantly tracking how well your controls are working and communicating the results to leadership.

This pillar is critical for making sure your framework stays effective over time. Regulations change, new business activities introduce new risks, and controls that were once solid can become outdated. It happens.

Effective monitoring involves:

- Regular audits of key processes.

- Tracking key performance indicators (KPIs), such as the time taken to complete compliant background checks.

- Establishing clear channels for employees to report potential compliance issues without fear.

This ongoing vigilance ensures your framework isn’t a “set it and forget it” project. It becomes a dynamic system that adapts to new threats, ultimately protecting your organisation day in and day out.

Navigating India’s Shifting Regulatory Environment

Let’s be honest: the ground beneath India’s regulatory world is in constant motion. For any business, standing still is the same as falling behind. This isn’t just a gradual change, either. It’s a rapid acceleration, fuelled by two powerful forces: the government’s aggressive digitalisation push and far more intense scrutiny from regulatory bodies.

Think of it like trying to build a solid house on shifting sands. Your old, reactive approach to compliance just won’t cut it anymore. Relying on a simple checklist of rules is like bringing a paper map to a high-speed car chase—you’ll be lost and overwhelmed in no time. A modern regulatory compliance risk management strategy has to be dynamic and always looking ahead.

This new reality is crystal clear in the financial services sector, where regulators are really flexing their muscles to enforce stricter governance. Just look at the Reserve Bank of India (RBI), which has seriously ramped up its enforcement. In the 2024 fiscal year, the monetary penalties it imposed more than doubled from the previous year, jumping from Rs 40.39 crore to a staggering Rs 86.1 crore. This isn’t random; it’s a calculated move to strengthen financial stability and protect consumers. You can get more insights on this compliance shift from KPMG.com.

Translating Directives into Daily Operations

Here’s where the real work begins. The biggest challenge for most organisations is figuring out how to turn complex master directions and dense circulars into practical, everyday actions. When a new notification on IT governance or data security lands on your desk, it’s not just a document for the legal team to file. It has real, tangible effects on your daily operations.

Take a look at what Indian regulators are focusing on:

- Data Security and Privacy: With the new Digital Personal Data Protection (DPDP) Act, how you handle personal data is under a microscope. This is especially true for the sensitive employee information you collect for background checks.

- Anti-Money Laundering (AML) and Fraud Prevention: Regulators are no longer satisfied with simple, rule-based checks. They’re demanding much more sophisticated systems to spot and report suspicious activities.

- IT Infrastructure and Cybersecurity: There’s a growing expectation for every business to have a robust cybersecurity framework to guard against a constant barrage of threats.

Each of these areas demands more than just a policy tucked away in a folder. They require concrete controls, continuous monitoring, and the ability to prove you’re compliant at a moment’s notice.

The core shift is from reactive, checklist-based compliance to proactive, automated, and continuous monitoring. The goal is no longer just to pass an audit but to build a resilient system that prevents failures before they happen.

The Critical Need for Modern Monitoring

This transition makes one thing painfully obvious: manual compliance processes are now a huge liability. Depending on spreadsheets and occasional manual reviews is just too slow and full of potential errors to keep up with the speed of regulatory changes. The sheer volume of data and the complexity of today’s rules make it impossible for human teams to manage it all without the right technology.

For example, imagine an HR department managing a bulk hiring drive. They have to ensure every single background check is done consistently and in full compliance with the law. Trying to track every step manually for hundreds of candidates isn’t just inefficient; it’s a breeding ground for compliance gaps. One tiny oversight could lead to a bad hire or a legal mess, exposing the company to serious risk.

This is exactly where automated systems become essential. They bring the speed, accuracy, and consistency needed to manage regulatory compliance risk management effectively. By automating routine checks and flagging issues in real-time, technology frees up your team to focus on strategic risk-fighting instead of drowning in paperwork. In India’s new regulatory era, this isn’t just about being more efficient—it’s about survival.

Critical HR Compliance Risks and How to Fix Them

The Human Resources department is the nerve centre of any organisation, but this central role also makes it a hotspot for compliance risks. Think about it: HR manages people, and that involves a ton of sensitive information and a dizzying maze of employment laws. A single misstep isn’t just a small error; it can unleash serious legal penalties, create massive operational headaches, and tarnish the employer brand you’ve worked so hard to build.

Effective regulatory compliance risk management in HR isn’t about chasing perfection—that’s a losing game. It’s about being prepared. It means putting on your detective hat, identifying the most vulnerable spots in your processes, and then building strong, practical defences to shield both the business and your people. For any HR pro, taking this proactive stance isn’t just a good idea; it’s a non-negotiable part of the job.

Unpacking Major HR Risk Zones

Let’s be honest, some HR functions are just riskier than others. It’s not a flaw; it’s just the nature of the data and the decisions involved. Getting a solid grip on these specific vulnerabilities is the very first step toward building a compliance strategy that can actually withstand pressure. The three areas that demand constant, eagle-eyed vigilance are data privacy, hiring practices, and statutory duties.

Here’s a closer look at these high-risk areas:

- Employee Data Privacy: In an age governed by laws like the Digital Personal Data Protection (DPDP) Act, how you collect, store, and process employee data is under an intense microscope. We’re talking about everything from Aadhaar numbers gathered during onboarding to the sensitive details that surface during background checks.

- Fair and Unbiased Hiring: Making sure your recruitment process is free from bias—both conscious and unconscious—is a huge legal and ethical responsibility. A seemingly harmless interview question or an inconsistent screening approach can quickly snowball into a discrimination claim.

- Statutory Compliance Duties: In India, employers are legally on the hook for managing social security contributions like Provident Fund (PF) and Employees’ State Insurance (ESI). Any failures in calculation, timely deposits, or reporting can lead to hefty financial penalties and legal battles.

Practical Fixes for Common Failures

Knowing the risks is one thing, but turning that knowledge into action is what really counts. You need battle-tested strategies to stop these risks from escalating into full-blown crises.

To make this crystal clear, here’s a breakdown of common compliance failures and the practical steps you can take to mitigate them.

Common HR Compliance Risks and Mitigation Strategies

| HR Risk Area | Potential Compliance Failure | Mitigation Strategy |

|---|---|---|

| Data Privacy | Storing unencrypted employee data or sharing it with unauthorised third parties. | Implement strong data encryption for all sensitive HR files. Adopt a strict access control policy, ensuring only personnel with a legitimate need can view employee data. |

| Hiring Practices | Inconsistent background screening leading to biased hiring decisions or bad hires. | Standardise your background verification process for all similar roles. Partner with a professional verification service to ensure checks are consistent, thorough, and legally compliant. |

| Statutory Duties | Incorrectly calculating or delaying PF and ESI contributions, leading to fines. | Automate payroll and statutory contribution calculations using reliable software. Establish a dual-approval system to verify amounts before processing payments to minimise human error. |

By putting these proactive measures in place, you transform high-risk processes into fortified strengths. Your HR function shifts from a purely defensive stance to one of strategic control and confidence.

The ultimate goal is to embed compliance into your daily workflows so that doing the right thing becomes the easiest and most natural path. This approach minimises human error and builds a culture of accountability.

Take background checks, for example. Relying on manual, ad-hoc methods is a recipe for disaster. Inconsistencies creep in all too easily, creating significant legal exposure. This is where specialised verification services become a powerful control measure. They ensure every candidate for a specific role undergoes the same rigorous, legally sound screening, which dramatically cuts down your organisational liability.

By systemising these critical checks, you’re not just improving compliance. You’re also making faster, more confident hiring decisions, which helps you build a stronger, more trustworthy workforce right from day one.

Using Technology to Get Ahead of Compliance Risk

In today’s world of compliance, clinging to spreadsheets and manual checklists is like trying to navigate a bustling highway with a paper map—you’re not just slow, you’re a liability. The sheer speed and volume of regulatory changes, especially in India, mean that old-school, manual methods are no longer just inefficient. They’re a massive risk.

This isn’t about replacing your team; it’s about empowering them. Technology acts as a force multiplier. It chews through the repetitive, data-heavy tasks that bog down your compliance experts, freeing them up to focus on what humans do best: strategy, nuanced judgement, and complex problem-solving. Investing in the right tools has moved from a “nice-to-have” cost to a powerful strategic advantage.

As we saw in 2024, Indian businesses faced an avalanche of regulatory challenges, forcing them to adapt or fall behind. Industry analysis shows a clear trend: companies are boosting their tech spend for compliance, with a huge focus on digital transformation. This means bringing in AI and Machine Learning to proactively spot risks, automate workflows, and slash the operational burden, as highlighted in a recent EY report on top regulatory compliance challenges for India Inc.

Harnessing AI and Automation

The real magic of modern compliance tech is its ability to predict and automate. AI and machine learning algorithms can sift through enormous datasets faster and more accurately than any human team possibly could. Think of them as your digital watchdogs, constantly on patrol for anomalies and potential red flags.

Here’s what that looks like in practice:

- Proactive Risk Flagging: An AI system can monitor transactions or communications in real-time. It automatically flags patterns that whisper of potential fraud or non-compliance long before they become a shouting match of an incident.

- Automated Reporting: Forget manually pulling data for audits. Technology can generate comprehensive, spot-on compliance reports with just a click, saving hundreds of hours of tedious work.

- Regulatory Change Management: Smart systems can track updates from regulatory bodies, alert your team to the changes that matter to you, and even suggest how to tweak your internal policies to stay aligned.

This proactive approach completely changes the game. It pulls your organisation out of a reactive “fix-it-when-it-breaks” mindset and into a forward-thinking strategy that sees threats coming and neutralises them.

By automating routine compliance tasks, you not only slash the risk of human error but also build a scalable framework that grows with your business—without piling on administrative costs.

Seamless Integration for Streamlined Workflows

One of the biggest wins with modern compliance tech is its ability to plug right into the systems you already use. Standalone tools that operate in their own little bubbles often create more headaches than they solve. A truly effective solution needs to talk seamlessly with your Human Resources Information System (HRIS) or Applicant Tracking System (ATS).

For instance, when you’re hiring, you can automatically trigger a compliant background check the moment a candidate hits a certain stage in your ATS. This kills manual data entry and ensures no crucial step gets missed. Information flows smoothly, processes are standardised, and compliance becomes an invisible, embedded part of your day-to-day workflow.

You can see exactly how SpringVerify API integrations help create these kinds of streamlined workflows for your HR processes.

Ultimately, weaving technology into your regulatory compliance risk management framework is about building a more resilient, agile, and intelligent organisation. It gives you the power to handle the intricacies of local Indian regulations while also staying aligned with global standards—a critical edge for any company looking to grow.

Building a Culture Where Compliance Thrives

Let’s be honest. You can have the most advanced frameworks and sophisticated tools in the world, but they’ll fall flat if your people aren’t on board. A truly successful regulatory compliance risk management strategy comes down to its most critical element: culture. This is about weaving compliance so deeply into your company’s DNA that it becomes a natural reflex, not a chore.

It all starts at the top. When leaders consistently talk about, prioritise, and model compliant behaviour, it sends a powerful signal across the entire organisation. This sets the stage for a culture where doing the right thing isn’t just expected—it’s the easiest and most supported choice.

Establishing Clear Accountability

For a compliance culture to truly take root, responsibility needs to be crystal clear. It’s not enough to just hand it off to the compliance department and call it a day. It has to be a shared mission where everyone understands exactly what part they play.

Think of it like a relay race. The compliance team might start with the baton, but it needs to be passed seamlessly to department heads, managers, and every single employee. Each person must know precisely when the baton is in their hands and what they need to do before passing it on.

This requires:

- Defined Roles: Clearly mapping out who is responsible for specific compliance tasks within each team. No grey areas.

- Performance Metrics: Tying compliance adherence to performance reviews to show it’s a core, non-negotiable part of the job.

- Empowerment: Giving employees the authority and resources they need to carry out their compliance duties effectively.

Delivering Training That Actually Sticks

We’ve all sat through those generic, tick-the-box training sessions. They’re boring, and they’re forgotten almost immediately. To build a lasting culture, your training has to be engaging, relevant, and continuous. Ditch the dry lectures on abstract rules and instead, use real-world scenarios that your team can actually relate to in their day-to-day work.

A truly compliant culture is one where employees feel safe to ask questions and raise concerns without any fear of blame or retaliation. It’s about creating trusted, confidential channels for open dialogue.

This proactive approach is non-negotiable, especially as regulations become more complex. Take the RBI’s Cyber Security Framework, for example. It now mandates that banks implement comprehensive strategies, including continuous security monitoring. This is a direct response to the new operational risks brought on by cloud technologies adopted in recent years, making robust internal vigilance more important than ever. You can learn more about how observability is helping Indian banks navigate compliance on Kloudmate.com.

When your team understands the “why” behind the rules, they stop being passive spectators and become active participants in protecting the business.

Frequently Asked Questions About Compliance Risk

Diving into regulatory compliance risk management can feel like opening a can of worms—it often creates more questions than answers, especially when you’re just starting out. Here, we’ll tackle some of the most common queries with straightforward, practical advice to help you solve real-world challenges.

Where Should Small Businesses Begin?

For a small business, the very idea of a full-blown compliance framework can feel like a mountain you’re not equipped to climb. The secret is to start small and focus on the areas with the highest impact first. Don’t try to boil the ocean.

Your first step is to identify your single most critical risk. For most companies, this usually boils down to either protecting employee data or ensuring financial accuracy.

Think of it this way: what one failure would cause the most immediate and severe damage to your business? Start there. Create a simple policy, train your team on it, and build momentum.

Once you’ve got a handle on that core risk, you can gradually expand your efforts. This step-by-step approach makes the whole process manageable. It ensures you’re protecting your most vital assets from day one without needing a massive budget to get going.

How Do I Balance Technology with Human Oversight?

Technology is a fantastic ally in compliance, but it’s no substitute for human judgement. The most effective strategies blend the unique strengths of both. Use technology for what it does best: churning through large volumes of data, automating repetitive tasks, and flagging anomalies with incredible speed and accuracy.

Here’s how you can strike the right balance in practice:

- Automate the Routine: Let your software handle the heavy lifting, like running initial background screenings or monitoring payroll for obvious errors.

- Empower Human Review: This frees up your team to focus on investigating the exceptions and complex issues flagged by the tech. A machine can spot a problem, but it takes a person to understand the context, ask the right questions, and decide on the best course of action.

This combination gives you the efficiency of automation without sacrificing the critical nuance that only a human expert can provide.

How Can We Stay Current with Changing Regulations?

Keeping up with regulatory updates can feel like a full-time job in itself. To stay ahead of the curve without getting buried in dense legal documents, focus on building three simple habits.

- Subscribe to Industry Updates: Follow reputable sources that do the hard work for you. Major consulting firms, specialised legal blogs, and government portals often provide easy-to-digest summaries of new regulations.

- Assign Ownership: Designate one person or a small team to be the official “tracker.” Their job is to monitor changes relevant to your industry and brief the leadership team every quarter.

- Lean on Compliant Partners: You don’t have to be an expert in everything. Work with service providers who are, like a verification partner who lives and breathes background check laws. This effectively outsources a piece of your compliance burden to someone who has it covered.

Ready to build a compliant hiring process without the guesswork? SpringVerify offers reliable, fast, and fully compliant background verification services designed for Indian businesses. Make informed hiring decisions with confidence.