Think of KYC Compliance and Fraud Prevention Day as a crucial, annual health check-up for your company’s financial well-being. It’s a designated day for businesses to pause, take stock, and seriously upgrade their defences against financial crime. For every business in India, this is a chance to transform compliance from a tick-box exercise into a real competitive edge.

Table of Contents

Why This Day Matters for Your Business

This day is much more than just a date circled on the calendar; it’s a vital initiative for keeping your business stable and maintaining its integrity. Whether you’re a large, established bank or a nimble fintech start-up, this day shines a spotlight on the constant battle against financial crime and why strong internal controls are non-negotiable.

Picture your company’s security framework as its financial immune system. Just as a person needs regular health checks to catch problems before they become serious, your business needs a dedicated moment to assess its defences. This day provides that perfect, structured opportunity to review and strengthen that ‘financial immune system’.

The Core Purpose of Observance

The main goal here is to shift businesses from a reactive mindset to a proactive one. Instead of waiting for a fraud incident to happen or a regulatory fine to land on your desk, companies are encouraged to use this day to actively test their systems, train their staff, and educate their customers. It’s an opportunity to ask some tough but necessary questions about your current setup.

This is especially important in India’s fast-paced economy, where digital transactions are skyrocketing—and so are the creative methods used by fraudsters. A solid commitment to KYC and fraud prevention is no longer just about satisfying regulatory bodies like the RBI. It’s now a fundamental part of building and keeping your customers’ trust.

A business that shows it’s serious about protecting customer data and assets doesn’t just stay on the right side of the law. It builds a reputation for reliability that attracts and keeps high-value clients. In a crowded market, trust is the ultimate currency.

Key Focus Areas for Businesses

Getting the most out of this day means zeroing in on a few key areas that form the foundation of any secure financial operation. These actions help turn awareness into real, tangible improvements:

- Auditing Existing Protocols: Take a hard look at your current KYC and Customer Due Diligence (CDD) processes. Where are the weak spots? Are there any glaring gaps that need plugging?

- Employee Training and Awareness: Run workshops to get your team up to speed on the latest fraud trends. Think phishing scams, identity theft, and new money laundering tactics.

- Technology and System Upgrades: Ask yourself if your current tech can actually spot sophisticated fraud patterns. It might be time to look at more advanced solutions.

- Customer Education Campaigns: Launch initiatives to teach your customers how to safeguard their accounts and spot potential security threats. An informed customer is your first line of defence.

By embracing the spirit of KYC Compliance and Fraud Prevention Day, your organisation can seriously boost its resilience, protect its hard-earned reputation, and help create a safer economic environment for everyone.

The Journey of KYC and Fraud Prevention in India

The story of KYC compliance in India is a perfect example of how regulations have to sprint to keep up with a fast-changing economy. It’s a journey that takes us from clunky, paper-based processes to the nimble, digital ecosystem we see today. Understanding this evolution helps businesses see why staying current isn’t just a tick-box exercise—it’s a strategic move.

In the early days, KYC was a completely manual affair. It meant physical documents, in-person visits, and long, long waits. Imagine a library where every new member had to show up with their original documents, and a librarian would painstakingly write their details into a ledger. The process was slow, riddled with human error, and a playground for fraudsters with forged documents.

The Shift to Digital Mandates

As India’s economy started picking up pace and the financial sector grew more complex, regulators like the Reserve Bank of India (RBI) knew the old paper-based system just couldn’t cut it anymore. The boom in digital banking and payments brought a whole new set of challenges, demanding a tougher, more scalable way to verify who people were.

This kicked off a series of mandates designed to standardise and digitise the KYC process. The aim was twofold: create a system that was easier for both businesses and customers, and one that was much harder for criminals to game. This regulatory push was really fuelled by the need to support new technology while simultaneously fighting off increasingly sophisticated fraud.

Compliance isn’t a static checklist you finish once. It’s a dynamic, moving target that changes with new tech and emerging threats. Adapting is key to survival and growth in India’s financial landscape.

Aadhaar and the e-KYC Revolution

The real game-changer in India’s compliance journey was the introduction of Aadhaar, the unique 12-digit identity number. This became the backbone for e-KYC (electronic Know Your Customer), a process that changed customer onboarding almost overnight. Suddenly, instead of stacks of paper, businesses could verify a customer’s identity instantly using their Aadhaar number and a quick biometric or OTP authentication.

The impact was massive. To give you an idea, in April 2023 alone, India saw over 14.95 billion Aadhaar-based e-KYC transactions. That staggering number shows just how deeply digital identity verification has been adopted across the nation. This shift streamlined onboarding for banking, insurance, and the stock market, making everything faster and more secure.

This digital leap drastically improved the efficiency of fintech compliance solutions and lightened the operational load on financial institutions.

The Central KYC Registry (CKYC)

The next big step forward was the creation of the Central KYC Registry (CKYC). This initiative was all about tackling the repetitive nature of KYC. Before CKYC, if you wanted to open a new bank account or get a new mutual fund, you had to go through the entire KYC process all over again.

CKYC fixed this by creating a centralised database where a customer’s verified KYC information is stored. The benefits are clear:

- No More Repetition: Customers only need to complete the KYC process once.

- Standardised Data: Information is stored in a single, uniform format, which means less confusion.

- Easy Access: Authorised institutions can pull up verified KYC data with the customer’s consent.

This journey—from manual paper trails to the interconnected CKYC ecosystem—shows a clear, forward-thinking progression. It tells us that Indian regulators are serious about building a framework that’s secure, efficient, and ready for what’s next, perfectly setting the stage for future kyc compliance and fraud prevention day initiatives.

Building a Modern KYC Compliance Framework

To really get behind the spirit of KYC compliance and fraud prevention day, a business needs a solid, up-to-date framework. Don’t think of this as just a single wall you put up. A better way to picture it is a series of smart, connected security checkpoints, where each one is designed to verify and truly understand who you’re doing business with. It’s a defence system built in layers, resting on three core pillars that work in tandem to keep you secure.

This layered approach starts with a basic identity check and then digs deeper to understand customer behaviour. The goal is to build an accurate risk profile for every single person you interact with.

Let’s break down exactly how these pieces fit together.

The First Pillar: Customer Identification Program

The Customer Identification Program (CIP) is the very foundation of your entire KYC structure. It’s the first gate every new customer has to pass through, no exceptions.

Think of it like being the host of an exclusive party. Your CIP is the security team at the front door. Their one job? To make sure every guest is exactly who they say they are before letting them in. It’s not about getting to know them personally just yet; it’s about checking their official ID to confirm their identity.

In the Indian business world, this means collecting and verifying specific, government-issued documents.

- Proof of Identity: This is usually a PAN Card or Passport.

- Proof of Address: Documents like an Aadhaar Card, Voter ID, or a recent utility bill work here.

- Recent Photograph: To make sure the face matches the name on the documents.

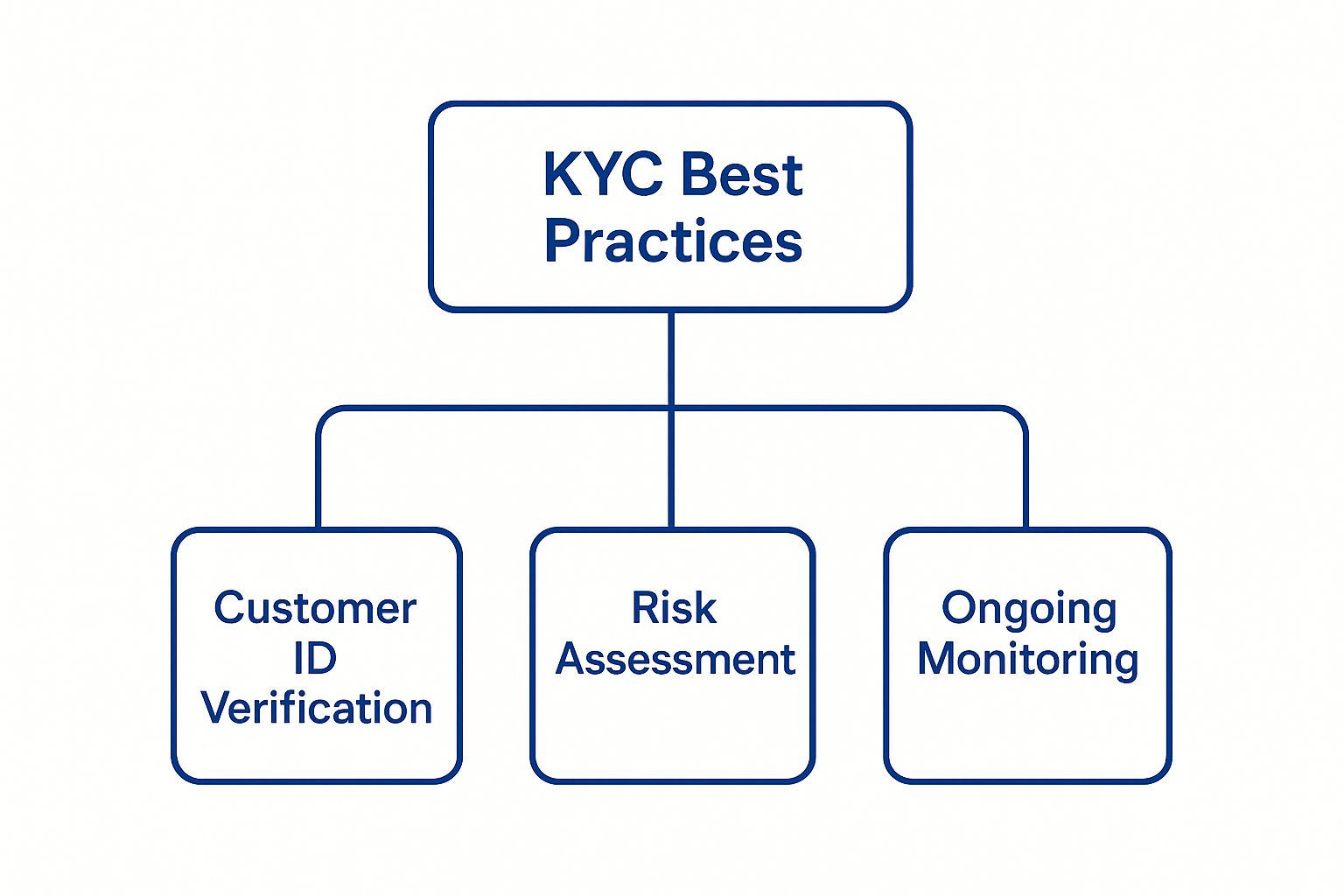

The objective of a CIP is simple but absolutely critical: to establish, with reasonable certainty, that you know the true identity of your customer. This step alone weeds out a surprising number of casual fraudsters.

This infographic shows how the core best practices grow from this initial verification step.

As you can see, once you’ve confirmed someone’s identity, the next logical steps are all about figuring out their risk level and keeping an eye on things over time. And that brings us to the next pillar.

The Second Pillar: Customer Due Diligence

Once your security team (CIP) has confirmed a guest’s identity at the door, the next phase is Customer Due Diligence (CDD). If CIP answers the question of who a customer is, CDD is all about understanding what they plan to do. This is where you graduate from a simple ID check to actually building out a risk profile.

To stick with our party analogy, CDD is like having your event staff mingle with the guests inside. They’re observing behaviour, getting a feel for why people are there, and trying to spot anyone who might cause trouble later.

Customer Due Diligence is the art of gathering just enough information to predict a customer’s likely behaviour. It helps you understand the kind of business they’ll be doing with you, so you can spot when their actions don’t match their profile.

For instance, if a salaried individual suddenly starts receiving huge, unexplained international money transfers, a good CDD process would flag that immediately. It’s about spotting activity that just doesn’t add up. This is a vital part of staying ahead of risks and is central to any good business compliance management strategy. The introduction of Video KYC (V-CIP) in India has made this much stronger, enabling real-time, face-to-face verification that adds a powerful layer of security to both CIP and CDD.

To better understand how these pillars function, let’s look at their distinct roles. The table below summarises the three essential components of a robust KYC programme, outlining what each does and when it’s used.

| Pillar | Primary Purpose | Typical Application |

|---|---|---|

| Customer Identification Program (CIP) | To verify a customer’s true identity against official documents. | At the very beginning of the relationship, during customer onboarding. |

| Customer Due Diligence (CDD) | To assess a customer’s risk profile based on their expected activities. | During onboarding and through periodic reviews for all standard customers. |

| Enhanced Due Diligence (EDD) | To conduct a deeper investigation into high-risk customers. | For specific categories of customers like PEPs or those from high-risk regions. |

As the table shows, each pillar has a specific job, building on the one before it to create a comprehensive defence.

The Third Pillar: Enhanced Due Diligence

Sometimes, a standard check just isn’t enough, especially for high-risk customers. This is where Enhanced Due Diligence (EDD) comes into play. Think of EDD as a much more intense, detailed level of scrutiny that you apply only when the stakes are higher.

Back at our party, EDD would be the dedicated security detail assigned to a VIP guest or someone who was flagged for acting suspiciously. This team does deeper background checks and keeps a much closer watch on that person throughout the event.

EDD is usually reserved for specific situations, such as dealing with:

- Politically Exposed Persons (PEPs): Individuals in prominent public positions.

- High-Net-Worth Individuals: Whose large transactions naturally require a closer look.

- Customers from High-Risk Jurisdictions: People operating in countries known for financial crime or terrorism financing.

This process means digging for more information, understanding where their wealth comes from, and monitoring their activity much more frequently. When you link CIP, CDD, and EDD together, you create a smart, dynamic framework that does more than just tick a regulatory box—it actively defends your business from threats as they evolve.

Solving India’s Customer Onboarding Puzzle

In India’s fast-paced market, businesses are walking a tightrope. On one side, you have the Reserve Bank of India’s strict KYC mandates, which are absolutely crucial for protecting our financial system. On the other, you have the modern Indian customer—especially the younger, tech-first generation—who won’t settle for anything less than a quick, seamless, and fully digital onboarding process.

This balancing act is the core challenge that comes into focus every kyc compliance and fraud prevention day. If you get it wrong, you create friction. We’re talking about those frustrating, time-consuming steps in a verification process that cause potential customers to just give up and go elsewhere.

A clunky onboarding process isn’t a minor hiccup; it’s a real drain on growth. Every single person who abandons an application because of complicated forms or slow verifications is a direct loss of revenue. This friction has become a major headache for the Indian financial sector.

Quantifying the Cost of Friction

The numbers here tell a pretty stark story. A recent survey found that a whopping 72% of Indian financial institutions lost potential customers over the last year, specifically because their KYC procedures were too long or intrusive. This problem is especially sharp among younger, digitally native clients who have zero patience for slow, invasive verification methods. It’s a clear sign of the tension between staying compliant and keeping customers happy. You can read more about these KYC challenges and their impact to get the full picture.

This isn’t just theory. It’s happening every day. Complicated interfaces and drawn-out document uploads lead to high drop-off rates, hitting the bottom line directly. Each unfinished application is a failure to turn an interested person into a loyal customer.

For today’s digital consumer, the onboarding experience is the first real interaction they have with your brand. A frustrating, slow, or confusing process doesn’t just lose a sale; it damages your reputation before the relationship even begins.

Slashing Friction with Technology

The good news is that we have powerful technology that can solve this puzzle without cutting any corners on compliance. The goal is to make the verification process so smooth that the customer barely even notices it’s happening. Modern tools can automate and simplify these vital steps, turning what was once a bottleneck into a real competitive advantage.

Here are three key technologies leading the charge:

- AI-Driven Automation: Artificial intelligence can instantly scan and verify documents like Aadhaar and PAN cards, check for signs of tampering, and pull out all the necessary information without anyone lifting a finger. This cuts down on human error and slashes verification time from days to just seconds.

- Biometric Verification: Using tools like facial recognition and liveness detection, businesses can confirm a customer’s identity with incredible accuracy. This proves the person opening the account is real and physically present, adding a strong layer of security that is also fast and easy for the user.

- Streamlined Video KYC (V-CIP): The RBI-approved Video Customer Identification Process has been a complete game-changer. It lets a trained official conduct a live, recorded verification call, capturing all the needed proofs in one quick session. This remote process gets rid of the need for in-person visits, making onboarding possible for anyone with a smartphone.

Reframing Compliance as an Opportunity

By bringing these technologies into the fold, businesses can dramatically cut the friction that causes customers to drop off. The process of streamlining identity verification checks with modern tools turns a regulatory headache into a strategic opportunity.

Instead of seeing KYC as just another hurdle to clear, forward-thinking companies see it as a chance to provide a genuinely better customer experience. A fast, secure, and hassle-free onboarding process doesn’t just tick a box for the RBI; it delights customers, builds trust from the very first interaction, and ultimately fuels business growth. On KYC Compliance and Fraud Prevention Day, this change in mindset is the key to winning over the next generation of Indian consumers.

The Future of Compliance with AI and Modern CKYC

The world of compliance is moving away from a simple, checkbox-ticking exercise. We’re now entering an era of proactive, intelligent systems, and it’s a change that couldn’t come soon enough. Looking past today’s standards, new developments in Artificial Intelligence (AI) and the modernisation of the Central KYC Registry (CKYC) are building a future where robust security and a great customer experience finally go hand-in-hand. This evolution is exactly what KYC Compliance and Fraud Prevention Day is all about—encouraging businesses to think ahead.

The whole point of this shift is to make compliance faster, more secure, and genuinely focused on the customer. Instead of treating verification as a necessary evil or a hurdle to jump, the aim is to weave it seamlessly and invisibly into the user’s journey. AI-powered tools are leading this charge, promising to slash onboarding times and finally put an end to the headache of submitting the same documents over and over again.

AI’s Role in Smarter Fraud Detection

Artificial Intelligence isn’t just a buzzword anymore; it’s a real, practical tool that is completely changing how we fight fraud. Old-school systems work on fixed rules, which clever fraudsters can easily figure out and bypass. AI, on the other hand, is dynamic. It learns and adapts, spotting subtle patterns and connections that a human analyst could easily miss.

Think of it like a security system that doesn’t just check names on a guest list but also watches behaviour to spot potential trouble before it starts. That’s what AI does, but with massive amounts of data in real-time.

- Behavioural Analytics: AI models can learn what ‘normal’ looks like for each customer. The moment an action deviates from that pattern—like a login from an odd location or a transaction that’s out of character—it gets flagged immediately.

- Link Analysis: Organised fraud is rarely a solo act; it often involves complex networks of fake accounts. AI excels at connecting the dots between seemingly unrelated data points to uncover these hidden rings that would otherwise fly under the radar.

- Predictive Risk Scoring: Rather than putting every customer through the same rigid checks, AI assigns a dynamic risk score to each person. This allows for a much smarter, risk-based approach where low-risk customers are fast-tracked, while high-risk ones get the extra scrutiny they need.

Of course, as we embrace AI in compliance, it’s vital to think about deploying it ethically and fairly. We can learn a lot from other fields, like the use of AI tools for reducing bias in hiring, which provides a great blueprint for building equitable AI solutions in our own industry.

Modernising the Central KYC Registry

The Central KYC Registry (CKYC) has long been a pillar of India’s compliance structure, and recent upgrades are making it more powerful than ever. The objective is to create a truly unified data ecosystem where the customer is in control—a huge step forward for everyone involved.

The next generation of CKYC is designed to put control back into the hands of the customer. It aims to make the process a “do-it-once, use-it-anywhere” experience, finally solving the problem of repetitive document submissions.

The Union Budget 2025 gave the CKYC framework a significant boost with several key upgrades. These include AI-powered duplicate detection using facial similarity, deep integration with DigiLocker for smooth document management, and new user dashboards. These dashboards let customers see who has accessed their KYC data and revoke that access in real-time. These changes are set to dramatically cut onboarding times—by up to 43%, according to analysis of AI-driven tools—and finally eliminate the frustrating cycle of resubmitting documents for customers with a KYC Identification Number (KIN). You can learn more about the CKYC enhancements and their impact to see how they’re reshaping the industry.

These aren’t just minor tweaks; they represent a total rethink of how KYC data is managed and shared.

- Mandatory Legacy Record Uploads: Financial institutions must now upload all their older KYC records to the central registry. This is creating a much more complete and unified database for the entire system.

- OTP-Based Consent: To pull a customer’s CKYC record, an institution now needs to get their explicit consent via a one-time password (OTP). This simple step gives individuals direct control over who sees their data and when.

- DigiLocker Integration: The link with DigiLocker means customers can provide verified digital documents with just a few clicks. It’s faster, more secure, and far more convenient than the old way of doing things.

Taken together, these advancements in AI and CKYC are building a future where compliance is no longer a burden. Instead, it’s becoming an efficient, secure, and user-friendly process. This vision is perfectly in tune with the forward-thinking spirit of KYC Compliance and Fraud Prevention Day, pushing us all toward a smarter, safer financial ecosystem.

Common Questions About KYC and Fraud Prevention

As businesses across India get serious about tightening their security, especially around kyc compliance and fraud prevention day, some very practical questions start to pop up. Let’s be honest, navigating the rules from bodies like the RBI and SEBI can feel like a maze.

This section is all about giving you direct, clear answers to the most common queries we hear. The goal is to help you move from theory to confident, real-world action.

What Is the Main Goal of KYC Compliance and Fraud Prevention Day?

The day’s main purpose is to spark proactive security upgrades across every industry. Think of it as an annual wake-up call for organisations to give their compliance frameworks a thorough review, update their fraud detection tech, and train their teams on the latest threats. It’s also about empowering customers with the knowledge to protect themselves.

This isn’t just a symbolic day on the calendar; it’s a powerful call to action. The real focus is on collectively reinforcing the entire financial ecosystem’s defences, making sure everyone sticks to regulatory standards while protecting businesses and their customers from financial crime.

Think of it as a nationwide fire drill for financial security. It’s a designated time for everyone to practise and refine their safety protocols, ensuring they are prepared before a real threat emerges, not after.

How Can Small Businesses Afford Effective KYC Processes?

Small businesses absolutely can implement strong KYC measures without breaking the bank. The key is to be smart and use scalable solutions. A great strategy is to partner with cloud-based identity verification services that offer pay-as-you-go pricing. This gives you access to crucial tools like digital ID checks and AML screening without a hefty upfront investment.

Adopting a risk-based approach is also a game-changer. This means you focus your most detailed checks on higher-risk customers and transactions, which is a much smarter way to use your resources. Plus, using government platforms like DigiLocker for document verification and training your staff to spot basic red flags are incredibly cost-effective steps. A digital-first onboarding process isn’t just cheaper; it’s fully compliant with today’s standards.

What Is the Difference Between KYC and AML?

Getting the distinction between Know Your Customer (KYC) and Anti-Money Laundering (AML) is fundamental. The easiest way to think about it is that AML is the entire rulebook for fighting financial crime, while KYC is a critical chapter within that book.

- Anti-Money Laundering (AML) is the big picture. It’s the complete framework of policies, laws, and controls a company puts in place to stop criminals from legitimising dirty money.

- Know Your Customer (KYC) is the hands-on process. It’s the specific set of actions you take to verify a customer’s identity and figure out their potential risk level by collecting and checking their documents.

In short, you perform KYC checks on your customers as a foundational part of meeting your much broader AML obligations. You can’t have an effective AML programme without a solid KYC process—it’s the bedrock it’s all built on.

How Does Video KYC Work in India?

Video KYC, or V-CIP (Video-based Customer Identification Process) as it’s officially known, is an RBI-approved method for onboarding customers remotely. It’s basically a live, encrypted video call between a trained official from your company and the customer. This process has completely changed the game for customer onboarding in India.

During this secure video chat, a few key things happen to confirm everything is legitimate:

- Live Photo Capture: The official takes a live snapshot of the customer to match against their ID photo.

- Original Document Verification: The customer has to show their original PAN card on camera, which the official verifies in real-time.

- Identity Confirmation: The official will ask a few questions to make sure the customer’s details are correct.

- Geo-tagging: The system captures the customer’s location to confirm the process is happening within India.

The benefits are huge. It’s incredibly fast, highly secure, and unbelievably convenient for the customer. Video KYC completely does away with the need for in-person visits, cutting down onboarding time from days to just a few minutes. It also often uses AI tools like liveness detection to catch sophisticated fraud attempts far more effectively than old-school paper methods ever could.

Ready to build a seamless and secure onboarding process? SpringVerify offers comprehensive background verification services, including instant KYC on WhatsApp, designed to help your business stay compliant and make hiring decisions with confidence. Discover how SpringVerify can protect your business and delight your new hires.